Handyman Liability & Business Insurance in Utah

Save Money with a local and knowledgeable Utah Commercial Insurance Agent!

Coverage Handymen Need

As a handyman, you most often work on people’s most valuable and cherished possession: their homes. Make sure you are protected for damage you may cause to that home or property with handyman insurance from Anderson Insurance Group.

Contractors E & O

General Liability

Workers’ Compensation

Tools & Equipment

Commercial Property/Installation Floater

Voluntary Property Damage

You can save up to 25% in discounts on Handyman insurance

You can pay for your insurance monthly or annually and you can cancel instantly at any time.

BASIC PACKAGE:

$500.00 yr/$47.45 Month

Get your license and get to work.

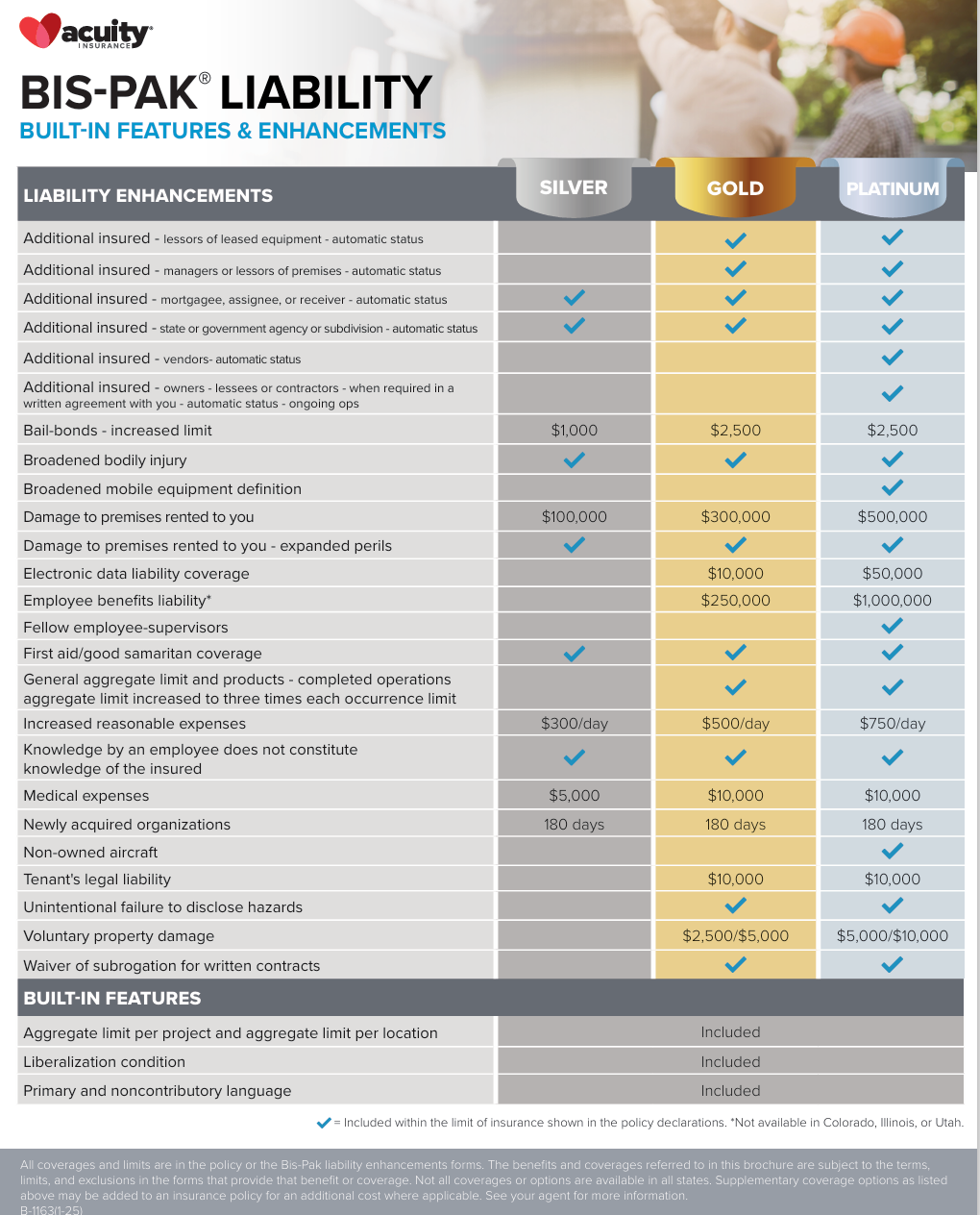

Silver Enhancements

GOLD PACKAGE:

$678.00 yr/63.64 Month

Most Popular: Certificates/Tools/High Limits

Gold Enhancements

PLATINUM PACKAGE:

$989.00 yr/$91.91 Month

Certificates/Tools/High Limits

Platinum Enhancements

Anderson Insurance Group offers Handyman Insurance Coverage through: Acuity Insurance, Auto-Owners, Cincinnati Insurance, and United Insurance Group.

Essential Insurance Coverage for Handymen and Independent Contractors

Get the right protection for your handyman business with comprehensive insurance coverage tailored to your needs. Anderson Insurance Group offers affordable policies that safeguard your work, equipment, and reputation.

Contractors E & O

Contractors E & O Protect your business from costly setbacks. What is Contractor's Errors & Omissions Insurance | Anderson Insurance Group

Get coverage for professional mistakes and negligence claims with Contractors E&O insurance. GL or CGL will not cover mistakes that you may make as a contractor and that is where Contractor’s E & O coverage comes into play.

General liability

General liability insurance is an important coverage for handymen providing financial protection in two key areas:

Bodily Injury to Third Parties (non-employees): If a client or a visitor to your worksite gets injured due to your operations, general liability can cover their medical expenses, legal fees, and potential settlements. For example, if a client trips over your toolbox and breaks their arm.

Property Damage to Third Parties: This covers damage you accidentally cause to property that doesn't belong to you. For instance, if you're installing a shelf and accidentally put a hole in the client's wall.

Workers’ Compensation

Workers’ Compensation is legally required if you employ staff. It covers medical bills and lost wages from work-related injuries. Workers’ Compensation | Anderson Insurance Group

Tools & Equipment

Your tools are your job security, protect them with sufficient insurance coverage from Anderson Insurance Group.

Voluntary Property Damage

Voluntary Property Damage provides coverage for unintentional damage to the real property of others while that property is under your Care, Custody, or Control. What is Voluntary Property Damage Coverage? | Anderson Insurance Group

Commercial Property/Installation Floater

If you need to protect building materials at your place or, at the property of a client, ask how to inexpensively protect them.

Why is handyman insurance important:

Licensing Requirements: To legally operate as a handyman in Utah, you must carry general liability insurance. Anderson Insurance Group can quickly provide the official proof of coverage required by DOPL so you can get licensed without delays. Handyman License & Insurance Requirements | Anderson Insurance Group

Client Expectations: It's very common for clients, especially those with larger projects or commercial clients, to ask for proof of insurance. They want to ensure that they won't be held financially responsible if something goes wrong. Having proof of insurance can help you win bids and build trust with potential clients.

Financial Protection: Without general liability insurance, a single accident or mistake could lead to significant out-of-pocket expenses for medical bills, property repairs, or legal defense costs, jeopardizing your business.