Hired & Non-Owned Auto Coverage in Utah // What Every Business Should Know

When your Utah business relies on employees to drive—even occasionally—you’re exposed to auto liability risks you may not be aware of. Whether an employee runs errands in their own car, picks up supplies, or rents a vehicle for a business trip, your business can be held responsible if an accident occurs. Hired & Non-Owned Auto (HNOA) coverage fills this gap.

Why HNOA Coverage Matters

Utah’s fast-growing and auto-dependent business environment means more mobility, more errands, and that means more risk. Even if you don’t own company vehicles, you may have employees driving their cars creating risk for your company.

Key Reasons Utah Businesses Need HNOA

- High Growth = More Driving – Startups, contractors, nonprofits, and home service providers rely heavily on employee mobility and sometimes, in their own vehicles.

- Liability Follows the Business – If an employee causes an accident while on the clock, your business can be liable.

- Personal Auto Policies May Not Cover Business Use – Many Utah drivers carry minimum limits that won’t fully protect your business. In addition, some personal auto policies will include strict exclusions for business use.

- Protection Against Costly Lawsuits – HNOA helps cover damage to other cars, medical expenses, and legal fees.

What is the Difference Between Hired Auto & Non-Owned Auto Coverage?

HNOA are added as separate endorsements to a general liability or commercial auto policy. It protects your business when vehicles you (the business) don’t own are used for work.

1. Hired Auto – Extends Liability to vehicles your business rents, leases, or borrows, for example:

- Extending liability to a rented truck to move equipment

- Extending Liability to a rental car for a business trip

- Extending liability to a vehicle from another company

Hired Auto Physical Damage – is the necessary coverage to extend physical damage – to that rented or borrowed vehicle. You will want to make sure you add this additional endorsement if you need “full coverage” for the vehicle you are renting. The insurance carrier will want to know the value of the vehicles you rent.

2. Non-Owned Auto – Employee- or volunteer-owned vehicles used for business tasks. Examples:

- Delivering products in an employee’s personal car

- Picking up supplies in a personal vehicle

- Sales calls in an employee’s personal automobile

- Volunteers using their own vehicles for nonprofit events

- A staff member picks up lunch for the office in their personal car

Important: HNOA protects the business, not the employee’s vehicle. Their personal auto insurance pays first; HNOA steps in if damages exceed their limits or if the coverage is denied.

What HNOA Coverage Includes

✔️ Liability Protection – Covers bodily injury or property damage caused by a non-owned or hired vehicle used for business.

✔️ Legal Defense Costs – Helps pay attorney fees and court expenses if your business is sued.

✔️ Excess Coverage – Activates after the driver’s personal auto insurance pays its portion.

❌ What HNOA Does NOT Cover

- Damage to an employee’s personal vehicle

- Physical damage to a rented vehicle (requires Hired Auto Physical Damage)

- Personal errands or non-business use

Do You Need HNOA Coverage?

- Do employees drive their own cars for work?

- Do you rent vehicles for business trips or projects?

- Do volunteers use personal vehicles?

- Would an unexpected auto-related lawsuit hurt your business?

If you answered yes to any of these, HNOA coverage is worth consideration.

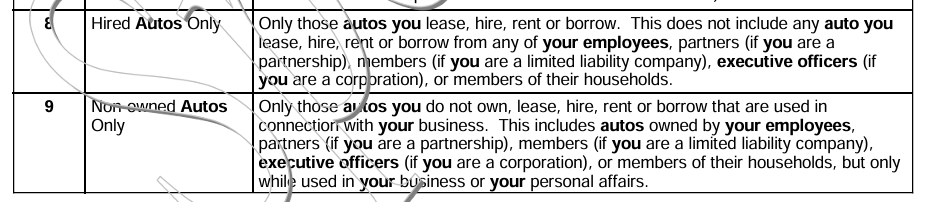

Here are a few additional details and a policy page for HNOA coverages:

Hired Auto can be found under symbol 8 of a commercial auto policy.

Non-owned Auto can be found under symbol 9 of a commercial auto policy.

For the complete endorsements including definitions, coverage, and exclusions, refer to your own policy or contact a knowledgeable agent at Anderson Insurance Group today.

Commercial Auto Insurance – Anderson Insurance Group